MarketWatch for May 2026

Markets moved higher in May, supported by strong corporate earnings and improving sentiment around easing geopolitical tensions. While volatility remained elevated, emerging markets led equity gains and corporate bonds outperformed government bonds.

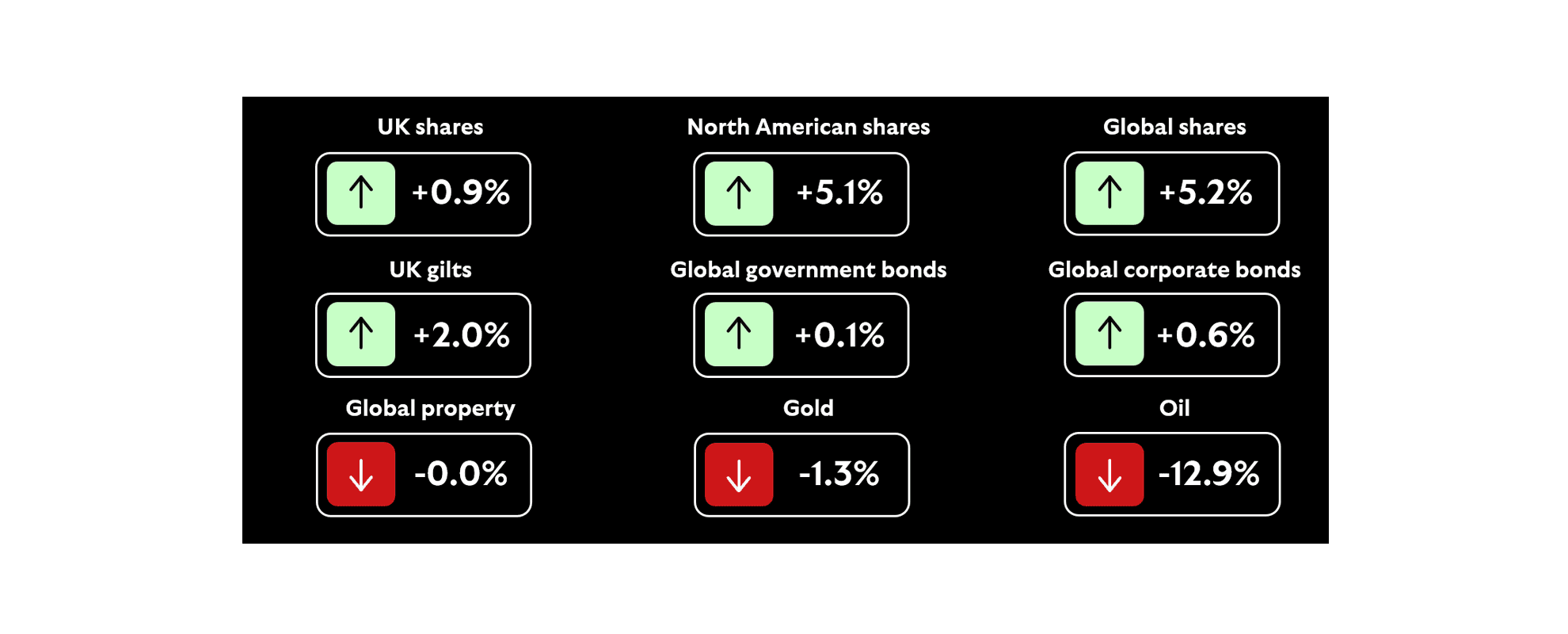

Markets made positive progress in May, supported by strong corporate earnings and growing hopes that tensions in the Middle East may ease. While volatility remained elevated at times, investor sentiment improved towards the end of the month.

In equities, emerging markets outperformed developed markets. Within fixed income, corporate bonds delivered stronger returns than government bonds.

United States

US equities advanced over the month, helped by a positive conclusion to the latest corporate earnings season. Technology stocks led the gains, although there were continued signs that investors are becoming more selective within the ‘Magnificent 7’ – favouring companies with stronger earnings momentum and clearer growth prospects.

Europe

Eurozone equities also moved higher, supported by encouraging corporate earnings. The information technology and consumer discretionary sectors were among the strongest performers. Inflation data showed some renewed pressure, with the annual eurozone rate rising to 3.0% in April from 2.6% in March, largely driven by higher energy costs.

United Kingdom

UK equities delivered modest gains but underperformed other regions. This was largely due to the market’s higher weighting towards energy and healthcare stocks, both of which declined over the month.

Japan

Japanese equities extended their recent upward trend. The market was led by AI- and semiconductor-related companies, supported by resilient domestic fundamentals and positive signals from US technology peers.

Emerging Markets

Emerging market equities were a standout performer, delivering strong gains and outperforming global indices. Sentiment was supported by continued enthusiasm around artificial intelligence and improving expectations of a potential US–Iran agreement. Gains were led by Korea and Taiwan, where semiconductor and memory stocks benefited from sustained AI-driven demand.

Fixed Income

It was an overall positive month for bond markets, although conditions remained volatile.

Government bond yields were heavily influenced by developments in energy markets and geopolitical tensions. Mid-month, fears of escalation in the Middle East pushed yields higher to multi-year peaks. However, this move reversed towards the end of May as optimism grew that a US–Iran agreement could be reached, easing concerns around both energy prices and stagflation.

Corporate bonds generated positive returns and outperformed government bonds. In the US, investment-grade credit led the way, while high-yield bonds lagged slightly, particularly in the financials sector. In contrast, eurozone high-yield bonds outperformed investment-grade counterparts on average.

Commodities

Commodities had a weaker month overall. Energy prices declined as the fragile ceasefire in the Middle East held and hopes increased for a more lasting resolution. Precious metals also fell, reflecting reduced demand for traditional safe-haven assets as risk sentiment improved.

Important information

Fees and charges apply.

The value of investments and the income from them can fall as well as rise and are not guaranteed. Investors may not get back the amount originally invested.

In preparing this article, we have used third party sources we believe to be reliable as at the date of writing, though we cannot guarantee the accuracy or completeness of the information.

Any views expressed are our inhouse views at the time of publication. This content may not be copied, quoted or circulated (in whole or in part) without prior written consent.